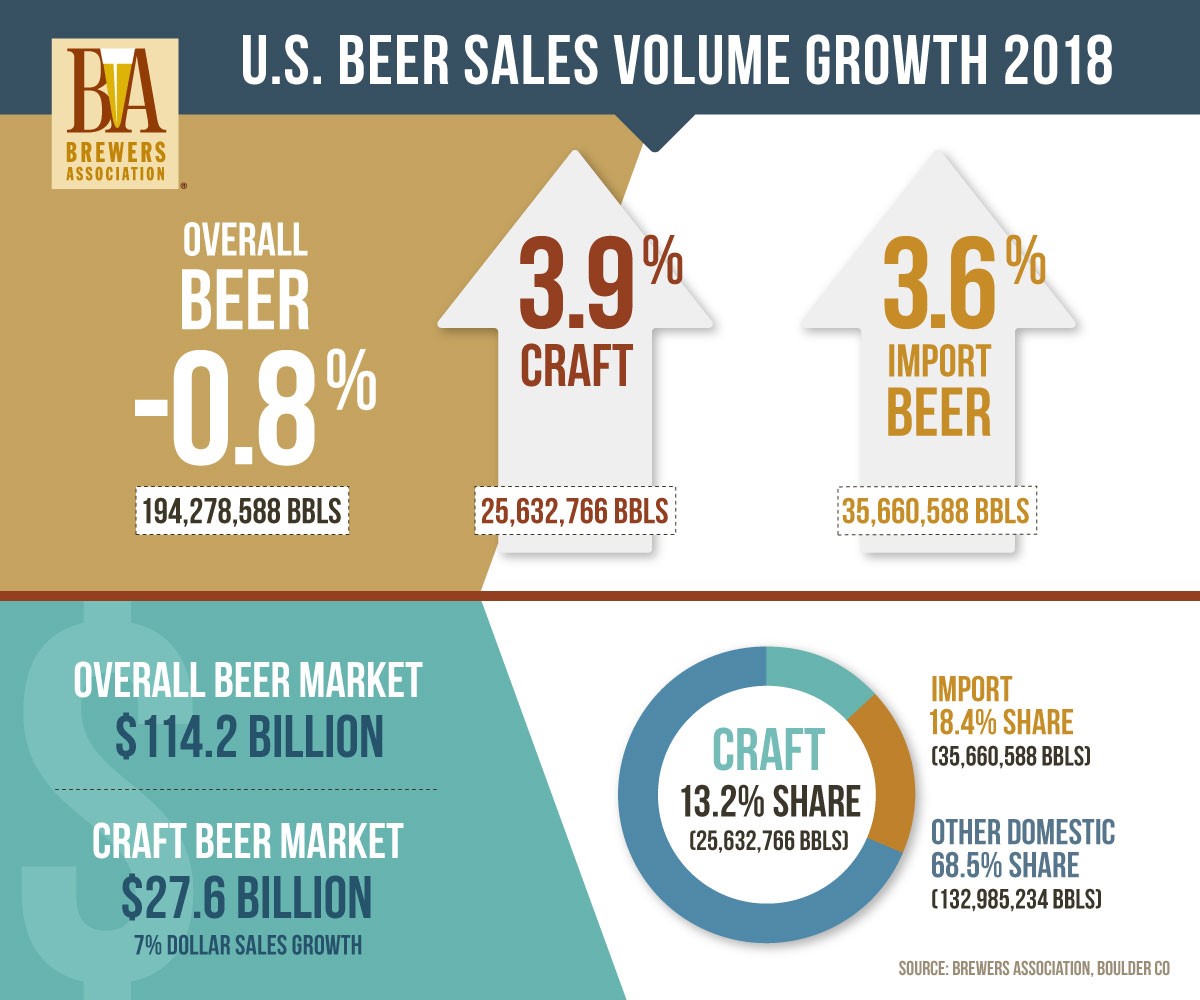

Small and independent American craft brewers have contributed $76.2 billion to the U.S economy in 2017, providing more than 500,00 total jobs. While the industry is clearly flourishing, brewery owners are often tasked with finding new ways to grow in such a competitive market. In fact, brewers who are looking to expand can spend considerable time researching a financing option that fits their needs.

Their solution is simple – the SBA 504 loan program.

Beer entrepreneurs have turned to the Small Business Administration’s (SBA) 504 program to expand their companies because the terms are typically significantly more attractive than conventional financing. The SBA 504 Loan is specifically designed to help small businesses grow. It features a below market, fixed interest rate and a 25-year term. In addition to the fantastic terms, the 504 loan is also attractive to brewers because they can finance high quality commercial brewery equipment in addition to facilities for their operation.

Advantages of securing an SBA 504 loan to purchase a building for your brewery

- Low down payment– Brewers can buy their facility with as little as 15 percent down. This down payment is considerably less than a conventional loan, which can be as high as 40 percent. This low down payment allows businesses to conserve more cash.

- Below market, FIXED interest rate – The SBA 504 loan allows business owners to lock in a below market rate. In a climate of rising rents, this gives entrepreneurs peace of mind knowing their rate won’t fluctuate due to lending conditions. Steady occupancy costs allows business owners to focus on their business operations.

- Long repayment term – The 504 Loan is fully amortized for 25 years, making loan payments more affordable and improving monthly cash flow.

- No balloon payments – Balloon payments mean there will be a large sum due at the end of the loan’s term OR refinancing will be required loan. This headache is avoided with the 504 loan.

- No additional collateral is required – The only collateral needed is the asset being acquired.

- Eligibility requirements– One of the best benefits of the 504 loan program is that MOST businesses are eligible. The business must be for-profit and must occupy at least 51 percent of the building. For new construction, the business must occupy at least 60 percent of the building.

- Equipment Financing– In addition to real estate, the SBA 504 loan program allows business owners to finance equipment. Brewers can include coolers, fermenters, kettles, etc., in their financing package. The equipment must have a useful life of 10 or more years. No appraisals are necessary, and taxes and installation fees can be included in the total project cost.

How Bear Republic Brewing Company Leveraged SBA 504 Real Estate Loans to Expand

Founded in 1995, Bear Republic Brewing Company began as a small family-owned business in Healdsburg, CA. With the help of several SBA loans, the business has expanded to multiple locations and has over 150 employees.

In 2006, Bear Republic secured their first SBA 504 loan to purchase a 14,136 square-foot facility in Cloverdale, CA. This property allowed the brewery to increase its capacity by more than 400 percent, expand distribution into 35 states and seven countries, and locally create more than 100 new jobs. The company has since expanded to take over not only the entire office park, but also the adjoining lot, allowing them to save on occupancy costs and increase production.

In 2017, Brewmaster and CEO Richard Norgrove, worked with TMC Financing to help Bear Republic secure another SBA 504 loan. With less than 20% down, Richard locked in the long-term, fixed-rate financing his company needed to continue its growth. The equipment and the acquisition of a hard liquor license allowed the Rohnert Park brew pub to offer unique food & specialty drinks to their patrons. Bear Republic’s innovative expansion efforts has led to 25 awards from the Great American Beer Festival, as well as many other medals from various organizations within the brewing industry.

In 2017, Brewmaster and CEO Richard Norgrove, worked with TMC Financing to help Bear Republic secure another SBA 504 loan. With less than 20% down, Richard locked in the long-term, fixed-rate financing his company needed to continue its growth. The equipment and the acquisition of a hard liquor license allowed the Rohnert Park brew pub to offer unique food & specialty drinks to their patrons. Bear Republic’s innovative expansion efforts has led to 25 awards from the Great American Beer Festival, as well as many other medals from various organizations within the brewing industry.

https://www.instagram.com/p/BlWp-rHnhN2/

Ultimately, SBA 504 loans are a great solution for growing breweries looking to stabilize their occupancy costs. Property acquisition through an SBA 504 loan is an accessible and affordable way to grow your business and solidify your financial security later in life.

The 504 Program & Support from a Certified Development Company

The SBA 504 loan is administered through nonprofit mission-based lenders, also known as Certified Development Companies (CDCs), such as TMC Financing. A CDC’s mission is to help match you with the loan product that will best support your growth, gain long-term success and create a positive impact on your community. CDCs guide business owners through the entire loan process and act as the owner’s advocate throughout the life of the loan.

CDCs can provide a prequalification analysis to small business owners, so they know their purchasing power and can act fast when they find the right opportunity. A prequalification letter can give you a leg up over other offers, which in the competitive Bay Area market, can make or break a deal. TMC can provide a free prequalification letter within 48 hours.

Learn More

You can find out more about using the 504 loan from one of TMC Financing’s 504 loan experts. TMC is an SBA Premier Certified Lender and a high-volume loan provider. With over 35 years of experience, TMC can help you find the financing that is best for you and guide you through the 504 loan process. Contact TMC Financing today.